Global Medical Display Market Overview

The Global Medical Display Market is experiencing steady growth as healthcare providers increasingly rely on high-precision display systems for accurate diagnostics and treatment planning. Medical displays, also referred to as medical-grade monitors, are specialized screens designed to render medical images with exacting clarity and adherence to strict regulatory standards. These displays are widely used in hospitals, diagnostic centers, surgical suites, and dental clinics to ensure accurate visualization of complex imaging data.

Medical displays support a variety of applications including diagnostic imaging, surgical procedures, patient monitoring, and dental imaging. Their high-resolution capabilities are critical in radiology, mammography, and other diagnostic procedures, reducing the risk of errors and improving patient outcomes. The market is driven by factors such as the increasing prevalence of chronic diseases, digitalization of healthcare, and demand for advanced visualization solutions.

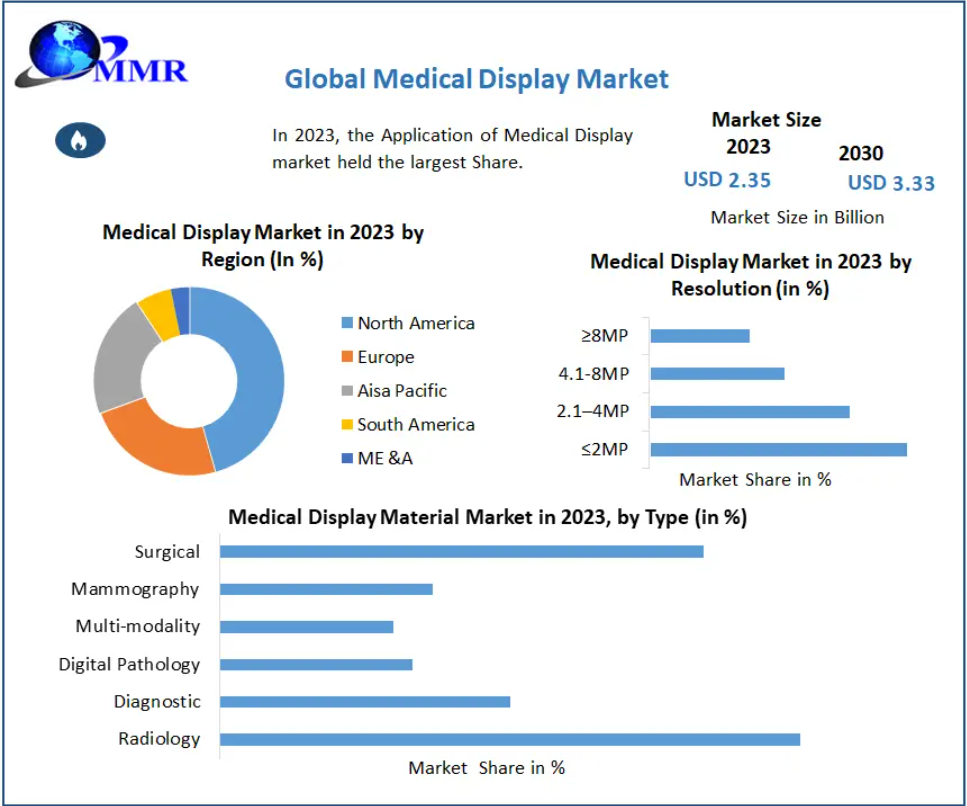

In 2023, the Medical Display Market was valued at USD 2.35 billion and is expected to grow at a CAGR of 5.10% from 2024 to 2030, reaching approximately USD 3.33 billion by the end of the forecast period. Key players including Barco NV, BenQ Medical Technology, Sony Corporation, and EIZO Corporation are driving market innovation through advanced display technologies, ergonomic designs, and integration of workflow optimization tools.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞:https://www.maximizemarketresearch.com/request-sample/3361/

Medical Display Market Scope

The report provides a comprehensive analysis of the Medical Display Market, covering market trends, technological advancements, regulatory influences, and competitive dynamics. It evaluates the market across multiple segments, including technology, panel size, resolution, display color, applications, and regions, to provide actionable insights for stakeholders.

Key growth drivers include the rising adoption of high-resolution displays in radiology and surgical settings, increasing investments in digital healthcare infrastructure, and continuous product innovation from leading market players. Challenges such as the high costs of advanced medical displays and ongoing maintenance requirements may constrain adoption in resource-limited settings. The study also highlights opportunities in emerging markets, driven by expanding healthcare infrastructure, growing awareness of advanced diagnostic technologies, and rising demand for precision imaging solutions.

Research Methodology

The insights in this report are derived from a blend of primary and secondary research methods to ensure accuracy and reliability:

- Primary Research: Engagements with industry experts, healthcare professionals, manufacturers, and distributors provided qualitative insights into market trends, adoption patterns, and technological preferences.

- Secondary Research: Information was collated from company reports, press releases, industry journals, government publications, and proprietary databases to validate market estimates and trends.

Market Sizing Approach: The study employed a bottom-up methodology, calculating market size by aggregating revenues from product types, applications, and regional markets. Data triangulation with secondary sources ensured consistency and reliability of the forecasted market figures.

Medical Display Market Segmentation

By Technology

- LED – Leading technology segment with a significant share due to superior brightness, energy efficiency, and image clarity.

- CCFL-backlit LCD – Widely used in legacy systems and cost-sensitive applications.

- OLED – Gaining traction for its high contrast ratios and accurate color reproduction, ideal for diagnostic applications.

By Panel Size

- ≤22.9-inch

- 23.0–26.9-inch – Largest market share in 2023 (~35.6%) due to suitability for most diagnostic workstations.

- 27.0–41.9-inch – Growing segment driven by high-resolution imaging and surgical visualization needs.

- ≥42-inch – Niche applications in advanced surgical suites and large-screen diagnostics.

By Resolution

- ≤2MP

- 2.1–4MP

- 4.1–8MP

- ≥8MP – High-end segment for critical diagnostic imaging such as radiology and mammography.

By Application

- Diagnostic – Largest segment due to the increasing need for accurate imaging and error reduction.

- Surgical – Growing adoption for intraoperative visualization and minimally invasive procedures.

- Dentistry – Adoption for digital dental imaging, treatment planning, and monitoring.

- Others – Includes veterinary, research, and laboratory applications.

By Display Color

- Color Display – Predominant segment due to demand in diagnostic and surgical imaging.

- Monochrome Display – Primarily used in radiography and specialized diagnostic applications.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞:https://www.maximizemarketresearch.com/request-sample/3361/

Regional Insights

North America

North America dominates the Medical Display Market, accounting for approximately 42% of the global share in 2023. The market is driven by a robust healthcare infrastructure, high healthcare spending, and strong adoption of digital diagnostic systems. The U.S. leads the region due to increasing investments in R&D, technological advancements, and rising prevalence of chronic diseases. Leading players such as Barco NV, BenQ Medical Technology, and EIZO Corporation actively innovate and introduce advanced displays to cater to growing clinical demand.

Europe

Europe is witnessing steady growth, with Germany, the UK, and France as primary markets. A combination of advanced healthcare facilities, regulatory compliance standards, and high awareness of medical imaging technologies drives market adoption. Companies such as Barco, STERIS, and Siemens Healthcare play a significant role in the region.

Asia-Pacific

The Asia-Pacific market is expanding rapidly due to increasing healthcare infrastructure, rising demand for diagnostic imaging, and awareness of advanced medical technologies. Key countries include China, India, Japan, and South Korea, with active participation from EIZO, Advantech, FSN Medical, and Sony Corporation.

Middle East & Africa

The region is growing steadily, driven by investments in healthcare modernization, establishment of private hospitals, and growing awareness of high-precision diagnostic tools.

South America

Emerging healthcare facilities in Brazil, Argentina, and Colombia create growth opportunities for medical display manufacturers. Market expansion is fueled by increasing adoption of digital imaging and diagnostic technologies.

Key Players

North America

- ViewSonic Corporation (USA)

- Novanta (USA)

- Double Black Imaging (USA)

- Dell (USA)

- HP (USA)

- FSN Medical Technologies (USA)

- Quest International (USA)

Europe

- Barco NV (Belgium)

- STERIS (UK)

- Siemens Healthcare (Germany)

Asia-Pacific

- Advantech (Taiwan)

- FSN Medical (South Korea)

- Axiomtek (Taiwan)

- COJE Display (South Korea)

- Alpinion Medical Systems Co., Ltd (South Korea)

- EIZO (Japan)

- Shenzhen Beacon Display (China)

- Jusha Medical (China)

- Sony Corporation (Japan)

- ASAHI ROENTGEN Co., Ltd. (Japan)

- LG Display (South Korea)

- BenQ Medical Technology (Taiwan)